Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2022-10-20 15:20:24-04

Research in Decentralized Identity Yields Confidential Data Storage

NEW YORK, Oct. 18, 2022 (GLOBE NEWSWIRE) — The Self-Sovereign Foundation, a nonprofit focused on equitable solutions for decentralized identity, has unveiled its Self-Sovereign Database. This critically needed software component stores sensitive data in a provably tamper-proof way. We all need to store personal data, and we all know it is not appropriately protected: trade secrets, family pictures, customer information, and healthcare data. Digital identity is not just about passwordless login and a driver’s license — it’s about all data. Because very soon, all data will be verified and credentialed.

The Self-Sovereign Database is a personal, privacy-respecting database management system for storing, searching and retrieving personal data so securely that even the storage provider cannot verify the identity or access the information. The Self-Sovereign Database is the ultimate secret data vault, a database powered by self-sovereign identity and verified credentials where only the individual is in control.

This breakthrough technology helps applications quickly achieve decentralization and data immutability without the slowness and expense of blockchain-based solutions while still being redundant, portable, and protected from breaches. The Self-Sovereign Database supports 256-bit AES encryption and optional FIPS security. The Foundation has started beta testing the integration of the Self-Sovereign Database with decentralized identity platforms and service providers and is seeking new partnerships. Currently supporting Microsoft Entra and EBSI, the database is W3C DID standard and interoperable.

About the Self-Sovereign Foundation

The Self-Sovereign Foundation is a nonprofit entity that empowers individuals with self-determination over personal data. The pillars of our Foundation are protecting confidentiality, ensuring accessibility, and equitable participation. Our mission is a future where users decide for themselves what information they share about themselves with different parties to preserve their privacy. For more information about our programs and research or to join our beta program, please visit us at https://selfsovereign.foundation.

Contact Information: Eric Stone President [email protected] 415-871-6485

Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2022-10-24 22:17:09-04

Passkeys are designed to replace passwords and allow seamless logins for consumers across devices and platforms.Makes online purchases easier for consumers, removes checkout friction for merchants.

SAN JOSE, Calif., Oct. 24, 2022 /PRNewswire/ — Today, PayPal announced it is adding passkeys as an easy and secure log in method for PayPal accounts. Passkeys are a new industry standard created by the FIDO Alliance and the World Wide Web Consortium that replace passwords with cryptographic key pairs, offering customers a simple and secure way to log in to PayPal based on technology that is resistant to phishing and designed so that there is no shared passkey data between platforms. The new PayPal log in option will first be available to iPhone, iPad, or Mac users on PayPal.com and will expand to additional platforms as those platforms add support for passkeys.

PayPal introduces passkeys as an easy and secure log in method for PayPal accounts.

A founding member of the FIDO Alliance, PayPal is one of the first financial services companies to make passkeys widely available to its users. This cutting-edge security standard is significant as passkeys address one of the biggest security problems on the web, which is the weakness of password authentication. Over 2.6 billion records were hacked in 2017 and of these hacks, 81% are estimated to have been caused by password stealing and guessing1. Many consumers recycle passwords across online services, which can not only be cumbersome but can also lead consumers to reuse the same, potentially vulnerable passwords across services. Passkeys are designed to replace passwords for an even more seamless and secure login experience with PayPal.

Passkeys will also help more consumers complete their purchases with PayPal – once PayPal users create a passkey, they won’t have to remember their password, allowing them to check out with greater ease. According to a recent survey of U.S. consumers, 44% of consumers have abandoned an online purchase because they forgot a password.2

“Launching passkeys for PayPal is foundational to our commitment to offering our customers safe, secure and easy ways to access and manage their daily financial lives,” said Doug Bland, SVP and GM, Head of Consumer, PayPal. “We are excited to provide our customers a more seamless checkout experience that eliminates the risks of weak and reused credentials and removes the frustration of remembering a password. We are making it easier for customers to shop online.”

How to Create a PayPal Passkey

Creating and using a passkey with PayPal is a quick and easy process on an Apple device. Once created, passkeys are synced with iCloud Keychain, ensuring a strong, private relationship between a customer and their device, and an easy sign-in experience for PayPal users with devices running iOS 16, iPadOS 16.1, or macOS Ventura.

Once existing customers log in to PayPal with a browser on desktop or mobile web using their existing PayPal credentials such as a username and password, they will have the option to “Create a passkey.”

Customers will then be prompted to authenticate with Apple Face ID or Touch ID. Then the passkey will be automatically created, and next time PayPal customers log in, they won’t need to use or manage a password again.

PayPal Passkeys Can Be Used to Log In on Any Device

If they have devices that don’t support passkeys yet, users can still use an iPhone to log in with a PayPal passkey. Users simply scan the QR code that will appear after they enter their PayPal User ID.

PayPal passkeys will start rolling out today to customers in the U.S.. PayPal passkeys will become available in additional countries early in 2023, and on additional technology platforms as they add support for passkeys.

About PayPal

PayPal has remained at the forefront of the digital payment revolution for more than 20 years. By leveraging technology to make financial services and commerce more convenient, affordable, and secure, the PayPal platform is empowering more than 429 million consumers and merchants in more than 200 markets to join and thrive in the global economy. For more information, visit paypal.com.

Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2022-11-10 23:18:09-05

New end-to-end solution has settled $1B in transactions to date with Checkout.com and will enable a global digital asset economy for merchants, entrepreneurs and creators.

Fireblocks (www.fireblocks.com), an easy-to-use platform to create innovative products on the blockchain and manage day-to-day crypto operations, announced today the public launch of its Payments Engine, a new suite of tools that will enable payment service providers (PSPs) with the ability to provide a blockchain agnostic, end-to-end solution for merchants, entrepreneurs and creators to accept, manage and settle digital asset payment transactions across any geography.

Early pilot partner Checkout.com, who was instrumental in supporting the development of the Payments Engine, has facilitated more than $1 billion in digital asset merchant settlements through their solution this year. Today, Fireblocks welcomes FIS, the largest merchant acquirer in the world, into its network of partners using the Payments Engine. FIS and its Worldpay solutions already provide card-to-crypto processing services for 4 of the top 5 cryptocurrency exchanges and was the first global merchant acquirer to offer USDC settlements. Together, the payment services providers collectively serve over a million merchants around the world.

“In the last several years, critical work has been done in the space to address pieces of the payments system,” said Michael Shaulov, CEO of Fireblocks. “From stablecoin settlement to cross-border payments to payouts for creators, we believe that the payments system must be addressed holistically, especially as we see digital assets continue to proliferate into mainstream technologies and the global economy. We have seen a tremendous amount of momentum from some of the biggest names in categories such as creator economies, streaming applications, and ride-sharing apps, who are actively thinking about more efficient ways to remit payments to marketplace participants.”

Following the acquisition of First Digital, which brought specialized digital asset payments capabilities to the Fireblocks’ platform, the newly launched Payments Engine provides a turnkey solution for businesses that want to integrate digital asset operations into existing or new products. Utilizing Fireblocks’ Payments Engine, PSPs will have a secure platform to deploy new digital asset payment rails, expanding their capabilities to accept, collect, payout, process and settle transactions using digital assets.

“The widespread use of stablecoins have made digital asset-based payments use cases very compelling for payments companies,” said Fireblocks Vice President and Head of Payments, Ran Goldi. “Fireblocks’ new Payments Engine will allow PSPs to offer and interact with a new breed of payments technology. We have had the privilege of working alongside the largest PSPs in the world to develop innovative fit-to-purpose solutions to support the next generation of payments products and services. We’re excited to roll out our vision for the payments space with our partners and showcase the results of these collaborative efforts with our customers in the upcoming months.”

With reports anticipating that over 75% of retailers plan to adopt digital asset payment services within the next two years, early movers in the payments space like Checkout.com and FIS have already begun taking advantage of Fireblocks’ Payments Engine to offer merchants the flexibility of 24/7 settlement, increasing cash flow, and reducing operational complexity.

“We’re enthusiastic about a wide-scale shift among enterprises and consumers towards digital payment systems,” said Nabil Manji, Head of Crypto & Web3 at FIS. “Together we will enable crypto-native and traditional businesses to accept, manage and settle digital assets so that they may choose their preferred currency for conducting business. This further builds on our relationship with Fireblocks, where we have already teamed to provide enterprise-grade digital asset investing and wallet technology to our capital market clients.”

In addition to stablecoin settlements, PSPs can use Fireblocks’ Payment Engine for:

Cross-border internal settlement — PSPs can now provide global, multinational companies ability to easily settle finances across multiple currencies with greater transparency

Creator/seller payouts — Enabling PSPs to offer payouts to marketplace participants faster and with more transparency in a way that is more suited to micropayments

Pay-ins — Allowing PSPs to enable their merchants to accept crypto as a payment method with significantly lower processing fees

“Across the globe, businesses, organizations, local governments, and individual consumers are all emphatically embracing new Web3 and digital payments technologies,” said Max Rothman, Head of Crypto & Digital Assets at Checkout.com. “To that end, through Checkout.com’s partnership with Fireblocks’ Payments Engine, we are able to pioneer new Web 3 solutions for our clients, such as our Stablecoin Settlement solution launched earlier this year. The result is faster, more affordable, and more secure transactions.”

Accessible via its UIs and APIs, Fireblocks’ Payments Engine provides a platform for PSPs to manage their merchants’ money flow in an easy and secure manner. Fireblocks is the highest-valued digital asset platform in the world, currently valued at $8 billion, and has also secured the transfers of over $3 trillion in digital assets.

Learn more about how the Fireblocks Payments Engine can power PSPs to build the next generation of digital asset services here: www.fireblocks.com/payments/

ABOUT FIREBLOCKS

Fireblocks is an enterprise-grade platform delivering a secure infrastructure for moving, storing, and issuing digital assets. Fireblocks enables exchanges, custodians, banks, trading desks, and hedge funds to securely scale digital asset operations through patent-pending SGX & MPC technology. They have secured the transfer of over $3 trillion in digital assets and have a unique insurance policy that covers assets in storage & in transit. For more information, please visit www.fireblocks.com.

The gap between fiat currency values and that of legal money, which is gold, has widened so that dollars retain only 2% of their pre-1970s value, and for sterling it is as little as 1%. Yet it is commonly averred that currency is money, and gold is irrelevant.

As the product of statist propaganda, this is incorrect. Originally established in Roman law, legally gold is still money and the states’ debauched currencies are not — only a form of credit. As I demonstrate in this article, the major western central banks will be forced to embark on a new round of currency debasement, likely to put an end to the matter.

Central to my thesis is that commercial bank credit will contract sharply in response to rising interest rates and bond yields. This retrenchment is already ending the everything bubble in financial asset values, is beginning to undermine GDP, and given record levels of balance sheet leverage makes a major banking crisis virtually impossible to avoid. Central banks which are already in a parlous state of their own will be tasked with underwriting the entire credit system.

In discharging their responsibilities to the status quo, central banks will end up destroying their own currencies.

So, why do we persist in pricing everything in failing currencies, when that will almost certainly change?

When the difference between legal money and declining currencies is finally realised, the public will discard currencies entirely reverting to legal money. That time is being brought forward rapidly by current events.

Why do we impart value to currency and not money?

A question that is not satisfactorily answered today is why is it that an unbacked fiat currency has value as a medium of exchange. Some say that it reflects faith in and the credit standing of the issuer. Others say that by requiring a nation’s subjects to pay taxes and to account for them guarantees its demand. But these replies ignore the consequences of its massive expansion while the state pretends it to be real money. Sometimes, the consequences can seem benign and at others catastrophic. As explanations for the public’s tolerance of repeated failures of currencies, these answers are insufficient.

Let us do a thought experiment to highlight the depth of the problem. We know that over millennia, metallic metals, particularly gold, silver, and copper came to be used as media of exchange. And we also know that the use of their value was broadened through credit in the form of banknotes and bank deposits. The relationships between legal money, that is gold, silver, or copper and credit in its various forms were defined in Roman law in the sixth century. And we also know that this system of money and credit with the value of credit tied to that of money, despite some ups and downs, has served humanity well ever since.

Now let us assume that in the absence of metallic money, in the dawn of economic time a ruler instructed his subjects to use a new currency which he and only he will issue for the public’s use. This would surely be seen as a benefit to everyone, compared with the pre-existing condition of barter. But the question in our minds must be about the durability of the ruler’s new currency. With no precedent, how is the currency to be valued in the context of the ratios between goods and services bought and sold? And how certain can one be about tomorrow’s value in that context? And what happens if the king loses his power, or dies?

Clearly, without a reference to something else, the king’s new currency is a highly risky proposition and sooner or later will simply fail. And even when a new currency has been introduced and linked to an existing form of money, if the tie is then cut the currency will struggle to survive. Without going into the good reasons why this is so, the empirical evidence confirms it. Chinese merchants no longer use Kubla Khan’s paper made out of mulberry leaves, and German citizens no longer use the paper marks of the early 1920s. But they still refer to metallic money.

Yet today, we impart values to paper currencies issued by our governments in defiance of these outcomes. An explanation was provided by the great Austrian economist, Ludwig von Mises in his regression theorem. He reasonably argued that we refer the value of a medium of exchange today to its value to us yesterday. In other words, we know as producers what we will receive today for our product, based on our experience in the immediate past, and in the same way we refer to our currency values as consumers. Similarly, at a previous time, we referred our experience of currency values to our prior experience. In other words, the credibility and value of currencies are based on a regression into the past.

Mises’s regression theory was broadly confirmed by an earlier writer, Jean-Baptiste Say, who in his Treatise on Political Economy observed:

“Custom, therefore, and not the mandate of authority, designates the specific product that shall pass exclusively as money, whether crown pieces or any other commodity whatever.”[i]

Custom is why we still think of currencies as money, even though for the last fifty-one years their link with money was abandoned. The day after President Nixon cut the umbilical cord between gold and the dollar, we all continued using dollars and all the other currencies as if nothing had happened. But this was the last step in a long process of freeing the paper dollar from being backed by gold. The habit of the public in valuing currency by regression had served the US Government well and has continued to do so.

The role of a medium of exchange

Being backed by no more than government fiat, to properly understand the role that currencies have assumed for themselves, we need to make some comments about why a medium of exchange is needed and its characteristics. The basis was laid out by Jean-Baptiste Say, who described the division of labour and the role of a medium of exchange.

Say observed that human productivity depended on specialisation, with producers obtaining their broader consumption through the medium of exchange. The role of money (and associated credit) is to act as a commodity valued on the basis of its use in exchange. Therefore, money is simply the right, or title, to acquire some consumer satisfaction from someone else. Following on from Say’s law, when any economic quantity is exchanged for any other economic quantity, each is termed the value of the other. But when one of the quantities is money, the other quantities are given a price. Price, therefore, is always value expressed in money. For this reason, money has no price, which is confined entirely to the goods and services in an exchange.

So long as currency and associated forms of credit are firmly attached to money such that there are minimal differences between their values, there should be no price for them either, other than a value difference arising from counterparty risk. A further distinction between money and currencies can arise if their users suspect that the link might break down. It was the breakdown in this relationship between gold and the dollar that led to the failure of the Bretton Woods agreement in 1971.

Therefore, in all logic it is legal money that has no price. But does that mean that when its value differs from that of money, does currency have a price? Not necessarily. So long as currency operates as a medium of exchange, it has a value and not a price. We can say that a dollar is valued at 0.0005682 ounces of gold, or gold is valued at 1760 dollars. As a legacy of the dollar’s regression from the days when it was on a gold standard, we still attribute no price to the dollar, but now we attribute a price to gold. To do so is technically incorrect.

Perhaps an argument for this state of affairs is that gold is subject to Gresham’s law, being hoarded rather than spent. It is the medium of exchange of last resort so rarely circulates. Nevertheless, fiat currencies have consistently lost value relative to legal money, which is gold, so much so that the dollar has lost 98% since the suspension of Bretton Woods, and sterling has lost 99%. Over fifty-one years, the process has been so gradual that users of unanchored currencies as their media of exchange have failed to notice it.

This gradual loss of purchasing power relative to gold can continue indefinitely, so long as the conditions that have permitted it to happen remain without causing undue alarm. Furthermore, for lack of a replacement it is highly inconvenient for currency users to consider that their currency might be valueless. They will hang on to the myth of its use value until its debasement can no longer be ignored.

What is the purpose of interest rates?

Despite the accumulating evidence that central bank management of interest rates fails to achieve their desired outcomes, monetary policy committees persist in using interest rates as their primary means of economic intervention. It was the central bankers’ economic guru himself who pointed out that interest rates correlated with the general level of prices and not the rate of price inflation. And Keynes even named it Gibson’s paradox after Arthur Gibson, who wrote about it in Banker’s Magazine in 1923 (it had actually been noted by Thomas Tooke a century before). But because he couldn’t understand why these correlations were the opposite of what he expected, Keynes ignored it and so have his epigonic central bankers ever since.

As was often the case, Keynes was looking through the wrong end of the telescope. The reason interest rates rose and fell with the general price level was that price levels were not driven by interest rates, but interest rates reacted to changes in the general level of prices. Interest rates reflect the loss of purchasing power for money when the quantity of credit increases. With their interests firmly attached to time preference, savers required compensation for the debasement of credit, while borrowers — mainly businesses in production — needed to bid up for credit to pay for higher input costs. Essentially, interest rates changed as a lagging indicator, not a leading one as Keynes and his acolytes to this day still assume.

In a nutshell, that is why Gibson’s paradox is not a paradox but a natural consequence of fluctuations in credit and the foreign exchanges and the public’s valuation of it relative to goods. And the way to smooth out the cyclical consequences for prices is to stop discouraging savers from saving and make them personally responsible for their future security. As demonstrated today by Japan’s relatively low CPI inflation rate, a savings driven economy sees credit stimulation fuelling savings rather than consumption, providing capital for manufacturing improvements instead of raising consumer prices. Keynes’s savings paradox — another fatal error — actually points towards the opposite of economic and price stability.

It is over interest rate management that central banks prove their worthlessness. Even if they had a Damascene conversion, bureaucrats in a government department can never impose decisions that can only be efficiently determined by market forces. It is the same fault exhibited in communist regimes, where the state tries to manage the supply of goods— and we know, unless we have forgotten, the futility of state direction of production. It is exactly the same with monetary policy. Just as the conditions that led the communists to build an iron curtain to prevent their reluctant subjects escaping from authoritarianism, there should be no monetary policy.

Instead, when things don’t go their way, like the communists, bureaucrats double down on their misguided policies suppressing the evidence of their failures. It is something of a miracle that the economic consequences have not been worse. It is testament to the robustness of human action that when officialdom places mountainous hurdles in its path ordinary folk manage to find a way to get on with their lives despite the intervention.

Eventually, the piper must be paid. Misguided interest rate policies led to their suppression to the zero bound, and for the euro, Japanese yen, and Swiss franc, even unnaturally negative deposit rates. Predictably, the distortions of these policies together with central bank credit inflation through quantitative easing are leading to pay-back time.

Rapidly rising commodity, producer and consumer prices, the consequences of these policy mistakes, are in turn leading to higher time preference discounts. Finally, markets have wrested currency and credit valuations out of central banks’ control, as it slowly dawns on market participants that the whole interest rate game has been an economic fallacy. Foreign creditors are no longer prepared to sit there and accept deposit rates and bond yields which do not compensate them for loss of purchasing power. Time preference is now mauling central bankers and their cherished delusions. They have lost their suppressive control over markets and now we must all face the consequences. Like the fate of the Berlin Wall that had kept Germany’s Ossies penned in, monetary policy control is being demolished.

With purchasing powers for the major currencies now sinking at a more rapid rate than current levels of interest rate and bond yield compensation, the underlying trend for interest rates is now rising and has further to go. Official forecasts that inflation at the CPU level will return to the targeted 2% in a year or two are pie in the sky.

While Nero-like, central bankers fiddle commercial banks are being burned. A consequence of zero and negative rates has been that commercial bank balance sheet leverage increased stratospherically to compensate for suppressed lending margins. Commercial bankers now have an overriding imperative to claw back their credit expansion in the knowledge that in a rising interest rate environment, their unfettered involvement in non-banking financial activities comes at a cost. Losses on financial collateral are mounting, and the provision of liquidity into mainline non-financial sectors faces losses as well. And when you have a balance sheet leverage ratio of assets to equity of over twenty times (as is the case for the large Japanese and Eurozone banks), balance sheet equity is almost certain to be wiped out.

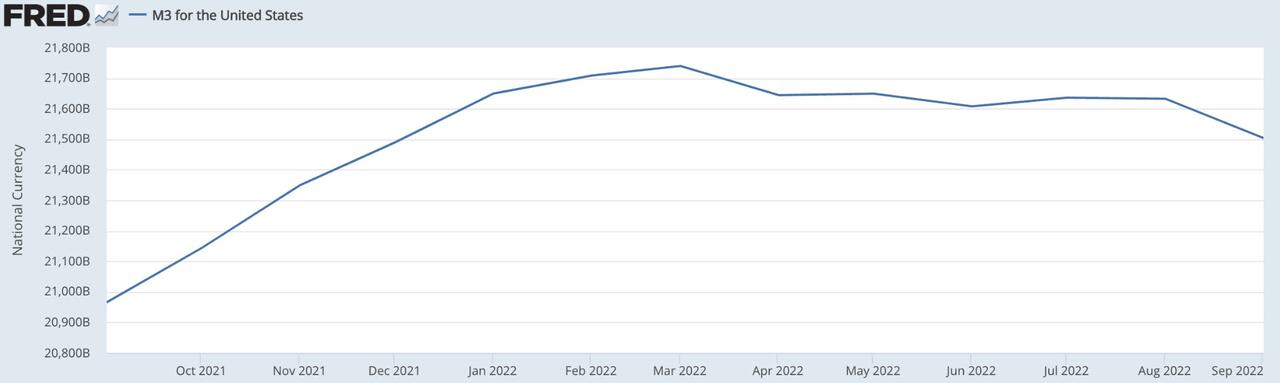

The imperative for action is immediate. Any banker who does not act with the utmost urgency faces the prospect of being overwhelmed by the new interest rate trend. The chart below shows that the broadest measure of US money supply, which is substantially the counterparty of bank credit is already contracting, having declined by $236bn since March.

Contracting bank credit forces up interest rates due to lower credit supply. This is a trend that cannot be bucked, a factor that has little directly to do with prices. By way of confirmation of the new trend, the following quotation is extracted from the Fed’s monthly Senior Loan Officers’ Opinion Survey for October:

“Over the third quarter, significant net shares of banks reported having tightened standards on C&I [commercial and industrial] loans to firms of all sizes. Banks also reported having tightened most queried terms on C&I loans to firms of all sizes over the third quarter. Tightening was most widely reported for premiums charged on riskier loans, costs of credit lines, and spreads of loan rates over the cost of funds. In addition, significant net shares of banks reported having tightened loan covenants to large and middle-market firms, while moderate net shares of banks reported having tightened covenants to small firms. Similarly, a moderate net share of foreign banks reported having tightened standards for C&I loans.

“Major net shares of banks that reported having tightened standards or terms cited a less favourable or more uncertain economic outlook, a reduced tolerance for risk, and the worsening of industry-specific problems as important reasons for doing so. Significant net shares of banks also cited decreased liquidity in the secondary market for C&I loans and less aggressive competition from other banks or nonbank lenders as important reasons for tightening lending standards and terms.”

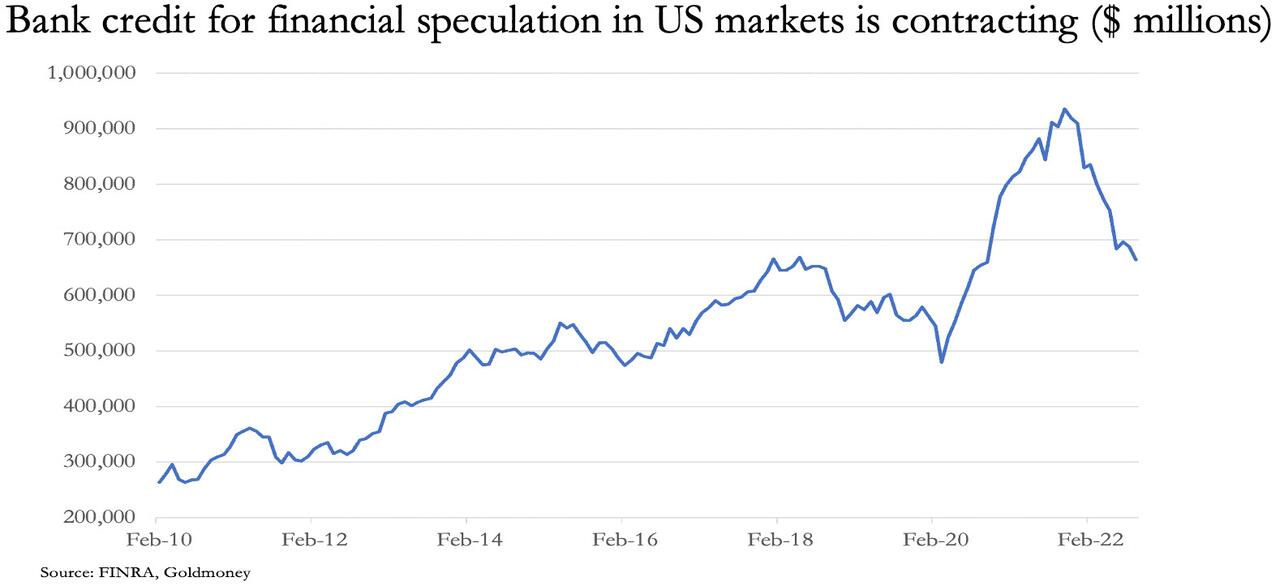

Similarly, credit is being withdrawn from financial activities. The following chart reflects collapsing credit levels being provided to speculators.

In the same way that the withdrawal of bank credit undermines nominal GDP (because nearly all GDP transactions are settled in bank credit) the withdrawal of bank credit also undermines financial asset values. And just as it is a mistake to think that a contraction of GDP is driven by a decline in economic activity rather than the availability of bank credit, it is a mistake to ignore the role of bank credit in driving financial market valuations.

The statistics are yet to reflect credit contraction in the Eurozone and Japan, which are the most highly leveraged of the major banking systems. This may be partly due to the rapidity with which credit conditions are deteriorating. And we should note that the advanced socialisation of credit in these two regions probably makes senior managements more beholden to their banking authorities, and less entrepreneurial in their big-picture awareness than their American counterparts. Furthermore, the principal reason for continued monetary expansion reflects both the euro-system and the Bank of Japan’s continuing balance sheet expansion, which feed directly into the commercial banking network bolstering their balance sheets. It is likely to be state-demanded credit which overwhelms the Eurozone and Japan’s statistics, masking deteriorating changes in credit supply for commercial demand.

The ECB and BOJ’s monetary policies have been to compromise their respective currencies by their continuing credit expansion, which is why their currencies have lost significant ground against the dollar while US interest rates have been rising. Adding to the tension, the US’s Fed has been jawing up its attack on price inflation, but the recent fall in the dollar on the foreign exchanges strongly suggests a pivot in this policy is in sight.

The dilemma facing central banks is one their own making. Having suppressed interest rates to the zero bound and below, the reversal of this trend is now out of their control. Commercial banks will surely react in the face of this new interest rate trend and seek to contract their balance sheets as rapidly as possible. Students of Austrian business cycle theory will not be surprised at the suddenness of this development. But all GDP transactions, with very limited minor cash exceptions at the retail end of gross output are settled in bank credit. Inevitably the withdrawal of credit will cause nominal GDP to contract significantly, a collapse made more severe in real terms when the decline in a currency’s purchasing power is taken into consideration.

The choice now facing bureaucratic officialdom is simple: does it prioritise rescuing financial markets and the non-financial economy from deflation, or does it ignore the economic consequences of protecting the currency instead? The ECB, BOJ and the Bank of England have decided their duty lies with supporting the economy and financial markets. Perhaps driven in part by central banking consensus, the Fed now appears to be choosing to protect the US economy and its financial markets as well.

The principal policy in the new pivot will be the same: suppress interest rates below their time preference. It is the policy mistake that the bureaucrats always make, and they will double down on their earlier failures. The extent to which they suppress interest rates will be reflected in the loss of purchasing power of their currencies, not in terms of their values against each other, but in their values with respect to energy, commodities, raw materials, foodstuffs, and precious metals. In other words, a new round of higher producer and consumer prices and therefore irresistible pressure for yet higher interest rates will emerge.

The collapse of the everything bubble

The flip side of interest rate trends is the value imparted to assets, both financial and non-financial. It is no accident that the biggest and most widespread global bull market in history has coincided with interest rate suppression to zero and even lower over the last four decades. Equally, a trend of rising interest rates will have the opposite effect.

Unlike bull markets, bear markets are often sudden and shocking, especially where undue speculation has been previously involved. There is no better example than that of the cryptocurrency phenomenon, which has already seen bitcoin fall from a high of $68,000 to $16,000 in twelve months. And in recent days, the collapse of one of the largest crypto-exchanges, FTX, has exposed both hubris and alleged fraud, handmaidens to extreme public speculation, on an unimaginable scale. For any student of the madness of crowds, it would be surprising if the phenomenon of cryptocurrencies actually survives.

Driving this volte-face into bear markets is the decline in bond values. On 20 March 2020, when the Fed reduced its fund rate to zero, the 30-year US Treasury bond yielded 1.18%. Earlier this week the yield stood at 4.06%. That’s a fall in price of over 50%. And time preference suggests that short-term rates, for example over one year, should currently discount a loss of currency’s purchasing power at double current rates, or even more.

For the planners who meddle with interest rates, increases in rates and bond yields on that scale are unimaginable. Monetary policy committees, being government agencies, will think primarily about the effect on government finances. In their nightmares they can envisage tax revenues collapsing, welfare commitments soaring, and borrowing costs mounting. The increased deficit, additional to current shortfalls, would require central banks to accelerate quantitative easing without limitation. To the policy planners, the reasons to bring interest rates both lower and back firmly under control are compelling.

Furthermore, officials believe that a rising stock market is necessary to maintain economic confidence. That also requires the enforcement of a new declining interest rate trend. The argument in favour of a new round of interest rate suppression becomes undeniable. But the effect on fiat currencies will accelerate their loss of purchasing power, undermining confidence in them and leading to yet higher interest rates in the future.

Either way, officialdom loses. And the public will pay the price for meekly going along with these errors.

Managing counterparty risk

Any recovery in financial asset values, such as that currently in play, is bound to be little more than a rally in an ongoing bear market. We must not forget that commercial bankers have to reduce their balance sheets ruthlessly if they are to protect their shareholders. Consequently, as over-leveraged international banks are at a heightened risk of failing in the new interest rate environment, their counterparties face systemic risks increasing sharply. To reduce exposure to these risks, all bankers are duty bound to their shareholders to shrink their obligations to other banks, which means that the estimated $600 trillion of notional over the counter (OTC) derivatives and on the back of it the additional $50 trillion regulated futures exchange derivatives will enter their own secular bear markets. OTC and regulated derivatives are the children of falling interest rates, and with a new trend of rising interest rates their parentage is bound to be tested.

We can now see a further reason why central banks will wish to suppress interest rates and support financial markets. Unless they do so, the risk of widespread market failures between derivative counterparties will threaten to collapse the entire global banking network. And that is in addition to existential risks from customer loan defaults and collapsing collateral values. Central banks will have to stand ready to rescue failing banks and underwrite the entire commercial system.

To avert this risk, they will wish to stabilise markets and prevent further increases in interest rates. And all central banks which have indulged in QE already have mark-to-market losses that have wiped out their own balance sheet equity. We now face the prospect of central banks that by any commercial measure are themselves financially broken, tasked with saving entire commercial banking networks.

When the trend for interest rates was for them to fall under the influence of increasing supplies of credit, the deployment of that credit was substantially directed into financial assets and increasing speculation. For this reason, markets soared while the increase in the general level of producer and consumer prices was considerably less than the expansion of credit suggested should be the case. That is no longer so, with manufacturers facing substantial increases in their input costs. And now, when they need it most, bank credit is being withdrawn.

It is not generally realised yet, but the financial world is in transition between economies being driven by asset inflation and suppressed commodity prices, and a new environment of asset deflation while commodity prices increase. And it is in the valuations of unanchored fiat currencies where this transition will be reflected most.

Physical commodities are set replace paper equivalents

The expansion of derivatives when credit was expanding served to soak up demand for commodities which would otherwise have gone into physical metals and energy. In the case of precious metals, this is admitted by those involved in the expansion of London’s bullion market from the 1980s onwards to have been a deliberate policy to suppress gold as a rival to the dollar.

According to the Bank for International Settlements, at the end of last year gold OTC outstanding swaps and forwards (essentially, the London Bullion Market) stood at the equivalent of 8,968 tonnes of bullion, to which must be added the 1,594 tonnes of paper futures on Comex giving an identified 10,662 tonnes. This is considerably more than the official reserves of the US Treasury, and even its partial replacement with physical bullion will have a major impact on gold values. Silver, which is an extremely tight market, is most of the BIS’s other precious metal statistics content and faces bullion replacement of OTC paper in the order of three billion ounces, to which we must add Comex futures equivalent to a further 700 million ounces.

On the winding down of derivative markets alone, the impact on precious metal values is bound to be substantial. Furthermore, the common mistake made by almost all derivative traders is to not understand that legal money is physical gold and silver — despite what their regulating governments force them to believe. What they call prices for gold and silver are not prices, but values imparted to legal money from depreciating currencies and associated credit.

While it may be hard to grasp this seemingly upside-down concept, it is vital to understand that so-called rising prices for gold and silver are in fact falling values for currencies. Some central banks, predominantly in Asia are taking advantage of this ignorance, which is predominantly displayed in western, Keynesian-driven derivative markets.

Perhaps after a currency hiatus and when market misconceptions are ironed out, we can expect legal money values to behave as they should. If a development which is clearly inflationary emerges, it should drive currency values lower relative to gold. But instead, in today’s markets we see them rise because speculators take the view that currencies relative to gold will benefit from higher interest rates. A pause for thought should expose the fallacy of this approach, where the true relationship between money and currencies is assumed away.

In the wake of the suspension of the Bretton Woods agreement and when the purchasing power of currencies subsequently declined, interest rates and the value of gold rose together. In February 1972, gold was valued at $85, while the Fed funds rate was 3.3%. On 21 January 1980 gold was fixed that morning at $850, and the Fed funds rate was 13.82%. When gold increased nine-fold, the Fed’s fund rate had more than quadrupled. And it required Paul Volcker to raise the funds rate to over 19% twice subsequently to slay the inflation dragon.

In the seventies, the excessive credit-driven speculation that we now witness was absent, along with the accompanying debt leverage in the financial sectors of western economies and in their banking systems. A Volcker-style rise in interest rates today would cause widespread bankruptcies and without doubt crash the entire global banking system. While markets might take us there anyway, as a deliberate act of official policy it can be safely ruled out.

We must therefore conclude that there is another round of currency destruction in the offing. Potentially, it will be far more extensive than anything seen to date. Not only will central-bank currency and QE expansion fund government deficits and attempt to compensate for the contraction of bank credit while supporting financial markets by firmly suppressing interest rates and bond yields, but insolvent central banks will be tasked with underwriting insolvent commercial banks.

At some stage, the inversion of monetary reality, where legal money is priced in fiat, will change. Instead of legal money being priced in fiat, fiat currencies will be priced in legal money. But that will be the death of the fiat swindle.

Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2022-12-06 02:34:07-05

The open-source Data Privacy Capability Model is a step-by-step guide to designing, running, and evaluating a strong data privacy program for any organization.

PHOENIX, ARIZONA, UNITED STATES, December 5, 2022 /EINPresswire.com/ — OCEG is pleased to announce the release of the new Integrated Data Privacy Capability Model (IDPM) and associated certification for Integrated Data Privacy Professionals. Together with a global review committee of privacy experts and the input of Singapore-based OCEG training partner, Straits Interactive, we have developed an open-source capability model that offers a detailed step-by-step guide to designing, running, and evaluating a strong data privacy program for any organization.

Carole Switzer, OCEG Co-Founder, and President notes, “Unlike other available resources and certifications, which generally outline the requirements of various data privacy regulations and tell you what you need to comply with, through this Capability Model we are seeking to help you understand how to meet those needs. Following the structure of our respected GRC Capability Model, we walk you through every stage of identifying relevant requirements for your organization, keeping track of where and how you are collecting and processing personal information, and ensuring that your data privacy program is transparent and auditable.”

The Capability Model is a free, open-source resource that anyone may download directly from the OCEG site.

“We are pleased to offer this important certification as an addition to our GRC Professional and GRC Audit certifications,” says OCEG Founder and Chair, Scott Mitchell, “and to include it at no additional cost for anyone who holds an OCEG All Access Pass. The AAP provides access to our premium resources and all our certification exams at one low cost, which ensures that every organization can have skilled and credentialed teams to address these critical needs.”

Said Kevin Shepherdson, CEO, Straits Interactive, “This Model, which we are honored to have authored with OCEG, offers something that has been missing in the information market for data privacy, that is, looking at privacy from an integrated governance, risk management and compliance perspective. The certification demonstrates an individual’s knowledge of how to build, run and assess an effective and agile data privacy program. As data privacy management becomes more challenging, it would be in every organization’s interest to ensure that its data privacy team and every manager of units with data privacy responsibilities, follow the model and obtain this valuable certification.”

Integrated Data Privacy Capability Model vs Other Privacy Certifications The Integrated Data Privacy Capability Model provides a roadmap for both GRC and privacy professionals. Those with specialized privacy certifications can now broaden their expertise into GRC as data privacy involves governing personal data, managing risks relating to personal data as well as complying with data privacy laws and regulations.

As for those who have the GRCP certification, this provides a roadmap for GRC professionals to cover data privacy which has become a big focus due to the General Data Protection Regulation and the introduction of many new data privacy laws around the world. By achieving the certification in the Integrated Data Privacy Capability Model, they have the option to then specialize in the area of data privacy and take on additional privacy certification qualifications.

Testimonials from Testers Testimonials from those who recently took the training have been encouraging and are shared here: “The course has a definitive guide for Data Protection Officers who are looking towards being operationally ready. What I learned the most would be the specific steps in preparing a robust data protection management program.”

“Relevant to my consulting practice going forward [the Model] provides a more detailed framework to advise clients on how to set up their privacy management plan.”

“The ‘learn and align’[component structure] provides a good way to frame the settings for our consulting with the management to align with their business objectives and enroll support.”

“The training provides in detail the steps required to set up a data privacy program (right from the start).”

“The training is very useful, how we combine data privacy knowledge and GRC perspective.”

“Found it useful to have understood the privacy framework in the larger context of GRC.”

About OCEG OCEG is a global nonprofit organization and community. We inform, empower, and help advance the careers of our 120,000+ members who work in governance, strategy, risk, compliance, security and audit. We created GRC to help every organization and every person achieve objectives, address uncertainty and act with integrity. This approach to business, and to life, is what we call Principled Performance®. For over 20 years, we’ve set the standards for GRC and the associated critical disciplines that comprise GRC. The foundational standards for GRC form the basis of OCEG’s GRC Capability Model (the “Red Book”) and additional OCEG capability models.

Straits Interactive Straits Interactive delivers sustainable data governance solutions that help organizations create trust in today’s data-driven world. As trusted advisors to SMEs, MNCs and data protection authorities in the region, we provide comprehensive competency, consulting and capability roadmaps in data protection and governance. We enable these competencies by partnering top universities in the region and international certification bodies to provide advanced diplomas, degrees and certification courses. Our hands-on advisory services, combined with our software-as-a-service solutions, help reduce risk and create value from data to help businesses achieve their digitalization and innovation objectives.

Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2023-01-11 01:55:21-05

LEHI, Utah, Jan. 10, 2023 /PRNewswire/ — Switch Reward Card, a blockchain-based financial services ecosystem that offers debit payment solutions for both traditional and cryptocurrencies, is excited to announce the following recent updates to its platform:

Switch’s Node Network Charter was passed and the Switch Blockchain went live in December.

Moved the Switch Black Card closed beta to open beta. The Switch Black Card currently has over 200 active users.

The Switch Trading Platform has over 120 users in closed beta. Beta Users can buy, sell and send cryptocurrencies, and has the ability to top-up or load the converted currencies to the Switch Black Card. Switch plans to add additional users to the test group in January.

Switch Reward Card Tap To Pay

In a December letter to the community announcing the launch of the blockchain, Switch Reward Card CEO, and former President of Discover Bank, Kathy Roberts said, “I feel fortunate to be making this announcement and to have kept that wonder about this emerging tech that will continue to change the world as it is being adopted faster than all previous technologies before it.”

Switch Reward Card President, COO and fellow co-founder Bradley Willden is excited about the versatility of the product suite: “The Switch platform has both custodial and non-custodial wallets giving our community members true ownership of their digital assets.”

CONTACT Switch Reward Card Scott Touchton Vice President of Sales and Marketing [email protected]

ABOUT Switch

Switch is a blockchain-based financial services ecosystem. The blockchain is empowered by a global decentralized node network where node licensees will be rewarded, by the blockchain, with Switch Digital Rewards. Switch offers debit payment solutions for both traditional and cryptocurrencies around the world.

This Press Release may contain forward looking statements that involve substantial risks and uncertainties. Forward looking statements discuss plans, strategies, prospects, and expectations concerning the business, operations, markets, risks, and other similar matters. There may be events in the future that we cannot accurately predict or control. Any forward-looking statement in this press release speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We do not plan to update or revise publicly any forward-looking statements except as required by law.

Rewards are not available for purchase from Switch. They are digital rewards earned in exchange for work and action on the Switch network. The digital reward is designed to have utility on the Switch platform for the purchase of Switch’s products and services. The digital reward is not an investment product and may never have any value outside of the Switch platform. Switch node owners should not expect to recognize any value from the digital reward other than its utility with Switch. Switch does not anticipate correlation between the digital reward value and Switch’s business activities.

No cryptocurrency is loaded onto the Switch Visa Card. All assets are converted to local fiat currency prior to loading on the Visa network. Switch provides financial services and is not a bank.

Follow Lions Gate - Digital Advocacy, filter it, and define how you want to receive the news (via Email, RSS, Telegram, WhatsApp etc.)

2023-01-13 22:57:06-05

Strategy will see major investments in quantum research, talent and commercialization

January 13, 2023 – Waterloo, Ontario, Quantum science and technologies are at the leading edge of research and innovation, with enormous potential for commercialization and game-changing advances, including more effective drug design, better climate forecasting, improved navigation and innovations in clean technologies. The Government of Canada is committed to supporting the continued growth of this emerging sector as it helps drive Canada’s economy and supports highly skilled, well-paying jobs.

Today, the Honourable François-Philippe Champagne, Minister of Innovation, Science and Industry, announced the launch of Canada’s National Quantum Strategy, which will shape the future of quantum technologies in Canada and help create thousands of jobs. Backed by an investment of $360 million committed in Budget 2021, the strategy will amplify Canada’s existing global leadership in quantum research and grow Canada’s quantum technologies, companies and talent.

Minister Champagne was joined at the launch by Dr. Raymond Laflamme, professor in the Department of Physics and Astronomy and Canada Research Chair in Quantum Information at the Institute for Quantum Computing at the University of Waterloo, and Dr. Stephanie Simmons, associate professor in the Department of Physics and Canada Research Chair in Silicon Quantum Technologies at Simon Fraser University and founder and Chief Quantum Officer of Photonic Inc. Drs. Laflamme and Simmons will serve as co-chairs of a new Quantum Advisory Council, which will provide independent expert advice on the implementation of the strategy.

The National Quantum Strategy is driven by three missions in key quantum technology areas:

Computing hardware and software—to make Canada a world leader in the continued development, deployment and use of these technologies

Communications—to equip Canada with a national secure quantum communications network and post-quantum cryptography capabilities

Sensors—to support Canadian developers and early adopters of new quantum sensing technologies

The missions will be advanced through investments in three pillars:

Research—$141 million to support basic and applied research to realize new solutions and new innovations

Talent—$45 million to develop and retain quantum expertise and talent in Canada, as well as attract experts from within Canada and around the world, to build the quantum sector

Commercialization—$169 million to translate research into scalable commercial products and services that will benefit Canadians, our industries and the world

Efforts under the strategy are already under way. To reinforce Canada’s research strengths in quantum science and help develop a talent pipeline to support the growth of a strong quantum community, the Natural Sciences and Engineering Research Council of Canada (NSERC) is delivering an investment of $137.9 million through its Alliance grants and Collaborative Research and Training Experience (CREATE) grants.

Mitacs will deliver $40 million to support the attraction, training, retention and deployment of highly qualified personnel in quantum science and technology through innovation internship experiences and professional skills development.

The Quantum Research and Development Initiative (QRDI), a new $9 million program coordinated and administered by the National Research Council of Canada (NRC), is being established to grow collaborative, federal quantum research and development. QRDI will bring government—offering expertise and infrastructure—and academic and industrial partners together to work on advancing quantum technologies under the three missions of the National Quantum Strategy.

To help translate quantum science and research into commercial innovations that generate economic benefits and support the adoption of made-in-Canada solutions by businesses, the NRC is receiving $50 million to expand the Internet of Things: Quantum Sensors Challenge program and roll out its Applied Quantum Computing Challenge program. As well, Canada’s Global Innovation Clusters are receiving $14 million to carry out activities as part of the Commercialization pillar.

In addition, the government’s flagship strategic procurement program, Innovative Solutions Canada, is receiving $35 million over seven years to help innovative Canadian small and medium-sized enterprises grow, scale up, develop intellectual property, export and create high-value jobs in the quantum sector.

The quantum sector is key to fuelling Canada’s economy, long-term resilience and growth, especially as technologies mature and more sectors harness quantum capabilities. Jobs will span research and science; hardware and software engineering and development, including data engineering; manufacturing; technical support; sales and marketing; and business operations. The government will continue working with Canada’s quantum community to ensure the success of not only the National Quantum Strategy but also the Canadian scientists and entrepreneurs who are well positioned to take advantage of these opportunities.

Quotes

“Quantum technologies will shape the course of the future and Canada is at the forefront, leading the way. The National Quantum Strategy will support a resilient economy by strengthening our research, businesses and talent, giving Canada a competitive advantage for decades to come. I look forward to collaborating with businesses, researchers and academia as we build our quantum future.” – The Honourable François-Philippe Champagne, Minister of Innovation, Science and Industry

Quick facts

According to a study commissioned by the NRC in 2020, it is estimated that, by 2045, the Canadian quantum industry, once quantum technologies take hold, will be a $139 billion industry (including all economic effects) and account for 209,200 jobs.

The Government of Canada has invested more than $1 billion in quantum since 2012. These foundational investments helped establish Canada as a global leader in quantum science.

The National Quantum Strategy was developed following thorough public consultations through stakeholder roundtables and an online survey.

A number of investments have already been announced through existing government programs, and additional partners are preparing their quantum programs for launch.

Innovative Solutions Canada has awarded four contracts valued at a total of $2.1 million to test quantum sensing, communications and computing solutions developed by Xanadu Quantum Technologies Inc., CogniFrame Inc., Photon etc. Inc. and Zero Point Cryogenics Inc.

To date, NSERC has awarded 17 grants valued at $1.5 million over three years and expects to announce further results of its quantum initiatives in the coming months, including the Alliance International Quantum grants, Alliance Quantum grants, Alliance Consortia Quantum grants and CREATE grants.

The NRC has launched Challenge programs to support collaborations with academia and industry that help drive commercial innovation and build on Canada’s position as a global leader in quantum technologies.

The Internet of Things: Quantum Sensors Challenge program is focused on developing revolutionary sensors that use the extreme sensitivity of quantum systems to enhance measurement precision and sensitivity rates and even expand the kinds of phenomena that can be measured.

The Applied Quantum Computing Challenge program is working to build capacity in quantum algorithms and software, as well as establish collaborative research and development projects with academia and industry to efficiently simulate complex physical systems, delivering new technologies for human health, climate change and advanced materials.

The governments of Canada and the United Kingdom have jointly launched a call for proposals open to organizations from Canada and the UK that wish to form project consortia for collaborative projects focused on developing innovative products, processes or technology-based services in the area of quantum technologies. The call is delivered by the NRC’s Industrial Research Assistance Program and Innovate UK.

{kind=link}

{kind=link}

{kind=link}